How to Begin Preparing Your Business For Sale

8 Steps to Selling Your Business

Introduction:

Selling your business is a once-in-a-lifetime event (for most, at least). Given the signifcance of this event and its lasting impact, it’s alarming how little time and effort many business owners spend on preparing the business for sale. Yes, buyers will want to know a lot about the business’ fnancial health with a focus on improvements that should be a top priority. But there are other factors and attributes that should be ‘polished’ up as well to obtain maximum value from your sale.

We know it can be hard to focus on these things when you’re also trying to keep the business running, all while maintaining confdentiality. This whitepaper will introduce you to the initial areas you should evaluate when preparing your business for sale, giving you a roadmap to get started. It is NOT an exhaustive list – it is a getting-started list.

Preparing Your Business For Sale

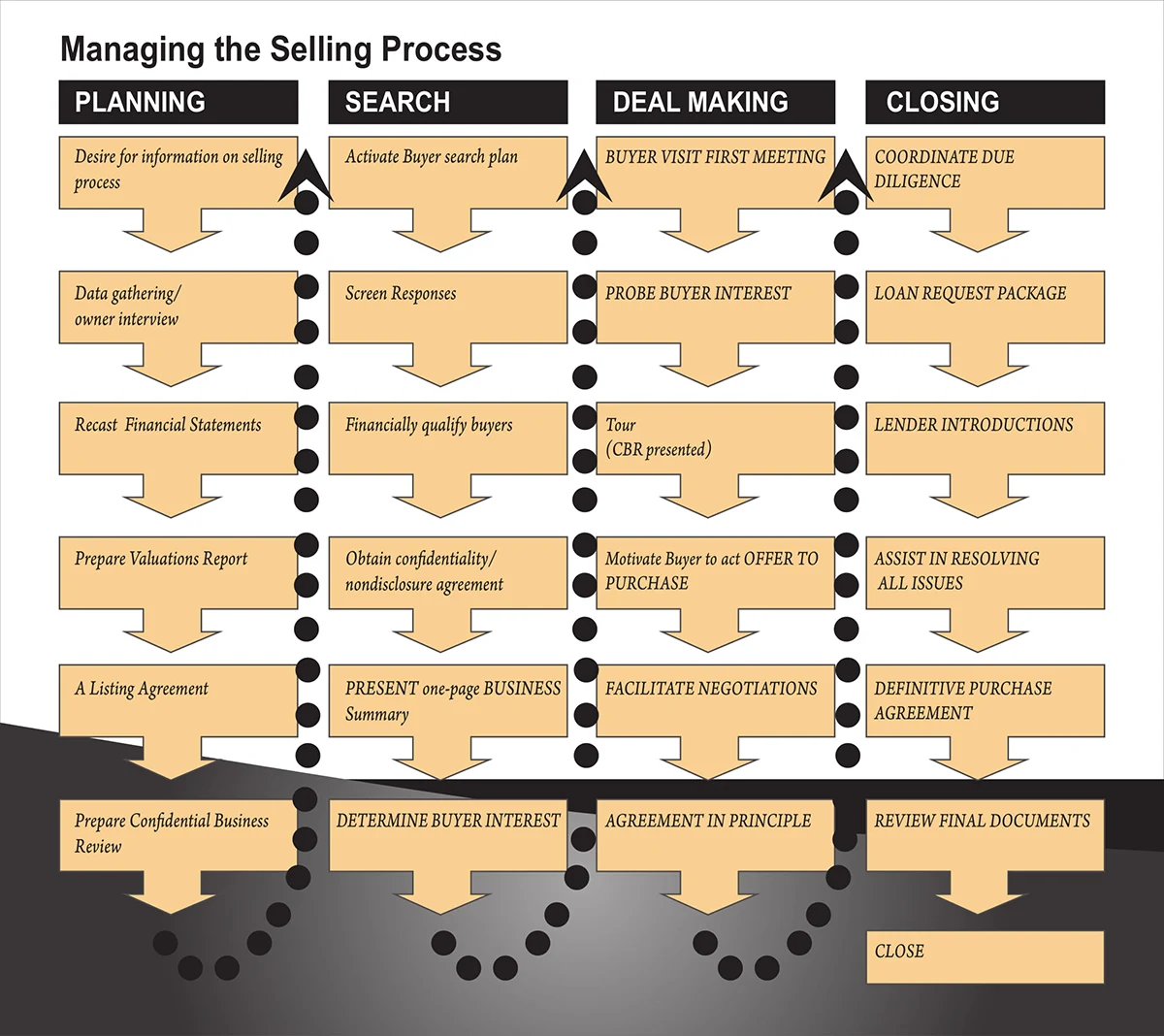

The Step by Step Process of Selling a Business in Florida

By FLORIDA BUSINESS BROKER | Published: DECEMBER 31, 2013

Florida business brokers are invaluable in guiding one through the following elements of the sale process:

Step 5: Legal & Tax Housekeeping

Your goal is to eliminate, or at least minimize, red fags associated with your business. Buyers will be immediately scared off if it’s apparent that the house just isn’t in order.

Follow this checklist to see which areas are good, and which need your attention..

- Ownership documents should be current and accurate.

- Have accountant evaluate if your current legal structure is optimal for the sale of your business.

- Make sure you have clear title to any major assets you intend to sell.

- Patents or licenses should be held by the business; check on the expiration dates.

- Correct any business licensing, regulation or compliance violations to the best extent possible.

- Get current on all taxes.

- Collect debts owed to you.

- Ensure building leases are current and assignable, and extend out at least

- 5 years. Resolve any outstanding lawsuits to the extent possible.

After addressing/correcting those that you can, the next step is outlining a strategy for how to present any remaining factors to potential buyers. Issues should be fully disclosed, but there may be opportunities to show buyers how corrective strategies or other resolution solutions have been deployed. For example, if you do have liens that cannot be paid off in advance, outline how they will be paid off through escrow at closing.

Step 8: What Will You Do Next

Besides just being fun to think about, outlining specifcally what you want your next phase of life to look like is actually very important for selling your business. Do you want to remain where you are located , or start traveling? Are you willing to stay involved with the business for a period of time, or do you want an immediate exit? How much time might you be willing to dedicate if you’re staying involved , for how long, and doing what activities ? What level and type of compensation would you seek? Would you be ok with someone else now having fnal decision making authority?

Many businesses need the current owner to stay around for at least a little bit, to facilitate the transition.For some sizes and types of businesses, that time frame could be extended to a couple of years. Complex businesses that are heavily relationship -dependent fall into this category, as well as those businesses that are more speculative in nature. Typically Independent Contractor Agreements , Non Compete Agreements and Earnouts are part of these scenarios , and they must be considered as part of the overall deal structuring.

Conclusion

You and your business broker need to work as a team to make your business look as good as possible, to get the highest sales price possible. Go section by section through your business, beginning with those elements outlined here, making a list of what needs work. Once you have the list, prioritize it then go to action. Your broker will offer objective insights along the way on how a buyer will be viewing things. While it will be hard work, it will pay off – literally.

Once you completed this getting started list, your broker will advise you of other areas that may need attention. The sooner you start ahead of your target sell-by date , the more improvements you can make, and the higher your closing price can be . The right Business Broker will optimize your benefit in terms of both asset return and expedience of a sale.